Why Most Young People Should Start Investing

The first in a three part series on why and how most people (not just young), should start investing — from the perspective of a young person passionate about investing.

The past year has seen financial events that will go down in history, from one of the fastest sell-offs since the Great Depression in March last year, to the incredible “everything bubble” that has ensued.

This has led to a flood of young people investing for the first time, from ‘Buy Now Pay Later’ (BNPL) companies Afterpay and Zip, to the Tesla bubble, to the influence of the subreddit “r/wallstreetbets” that is still going on and the titanic rise of meme-coins like Dogecoin and Safemoon.

I’d be lying if I said I wasn’t disappointed in missing out on potentially increasing my initial investment by over 10x. But at the same time, we have to keep in mind that for every millionaire’s story that we hear, there are likely many more who have lost money buying at the peak, trading too much or getting scammed. And honestly, that might even be a good thing. This is because by getting their hands dirty in investing and the memes that come along with it, they are increasingly likely to learn a thing or two about what style of investing suits their personal and financial goals. It would be even greater for them to understand the considerably more strategic advantage of thinking long-term, which I hope to express in this series of blog posts!

The Basics of Investing

What is investing?

Investing is the process of buying other assets with money, with the goal of getting “gainz” (or more money back). Some of the most common assets are “stonks” or shares (owning a small percentage of a company), property, bonds (large loans often issued by governments and businesses), commodities such as gold, and more recently, cryptocurrencies such as Bitcoin.¹

There are two main ways you can get money from these assets:²

- The asset will increase in value, so they can be sold to someone else at a higher price than you bought, the difference of these prices being your profit or “gainz” (capital gains).

- They will return a stream of money (income), such as receiving rent from a property you own or perhaps dividends from a share.

How is investing different to trading?

You’ve probably heard the word “trading” being thrown around with “investing”, and you might have thought they were the same thing.

Although, trading is a form of investing, the main distinction I would like to highlight is that trading generally focuses on making short term investments (usually holding an asset for under a year and can be as little as minutes or even seconds in the case of day traders on the stock market), profiting from market volatility (relatively short changes in price).³

On the other hand, investing is characterised as being more longer term focused (often holding assets for decades), thus usually requiring less monitoring and thus being safer. This is because investing generally relies upon the assumption that the economy and businesses will grow over the long run, which has been occurring for centuries, thus the value of assets which are at least partially underpinned by this movement increases.

So, investors have more time and resources to make their decisions, while traders have to make more time-sensitive and less evidence-based judgements (more on this in Part 2).

Why Most People Should Have Started Investing Years Ago

We’ve all heard of investing in some form, and may have just dismissed it as something that we’ll work out when we’re older or just as “something that isn’t for me”. However, I see this as being one of the biggest missed opportunities, especially for young people, as smart investing can lead to many positive changes.

Inflation — The Biggest Threat to Your Wealth

When thinking about the importance of investing, it might be helpful to cast your mind back to those days of Economics, where you studied inflation (don’t worry if you didn’t do it, I’ll explain the basics here).

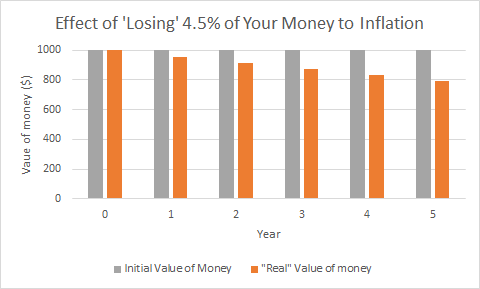

Inflation is the sustained increase in the prices of general goods and services. In other words, you would need to use more money to buy the exact same good than you did due to the increase in inflation. So, let’s just say you left all your spare money in your savings account at the bank. Now, you’d be lucky enough to get 0.5% of interest in Australia, and if you use the annual inflation rate at 1.1% at the end of March 2021, that would mean you are losing 0.6% of the value of your money by just leaving it there. At face value, that seems like nothing, but it does add up!

Luckily, we don’t live in a time when inflation totaled 98%, like in the US in the 70s. But, if we were to take the most up to date inflation numbers in the US (as the Australian statistic hasn’t come out at the time of writing), which was 5% for the year ending in May, we can see the devastating effects of this on your money. If you were to get the same amount of interest (0.5%) and inflation (5%) was to remain the same over a 5 year period, $1000 would be losing about 4.5% of its value annually. This would make the buying power of the money be less than $800, or the equivalent of being able to buy 20% less with the same amount compared to 5 years ago!

This explanation is simplified and unlikely to occur for this long of a period. But, you should keep in mind that due to the high safety of leaving your money in the bank, you won’t receive any significant returns on your money and it is likely to be worth less over time due to inflation.⁴

The Solution to Inflation

The eighth wonder of the world. Also known as compound interest.

Einstein is often attributed to having said this, although it was likely just a quote made-up by advertisers to make their financial products sound more impressive. Nonetheless, it might as well be the ‘eighth wonder’, due to its ability to exponentially grow your wealth over time (and get a higher return than you would from leaving it at the bank)!

Hamish Douglas, one of Australia’s most renowned and successful investors, has a favourite quote of Benjamin Franklin, one of the founding fathers of the US.

Money makes money, and the money money makes, makes more money.

He is describing compound interest, which occurs when the interest or return you get from holding an asset such as money in a savings account, is added to the initial amount you put in when calculating the next interest you receive. This creates a snowballing effect of more money each time you receive a return, as long as you give a bit of time for the effect to work.

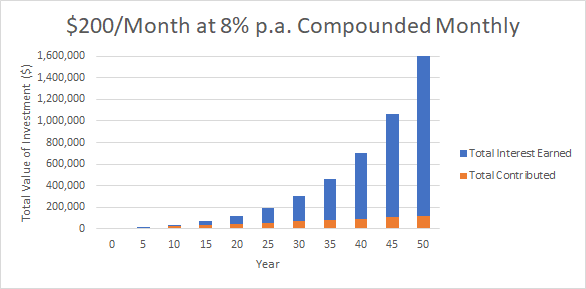

Starting young also comes with the advantage of building good financial habits, which can accelerate the effect of compounding. For example, if you set a goal of saving just 10% of your income to invest for your working life, as you progress in your career and become a more valuable employee, the regular deposit used in the example will increase over time, and you can see how this can significantly increase the end amount.

For instance, if you saved $200 a month (which would in reality likely increase over time — see previous paragraph), and put it into an asset that earned an interest rate of 8% (the average inflation adjusted stock market return in the US over the past 90 years or so)⁵ and you did this for 50 years (where if you are in your 20s now, you would have hopefully retired by then), your investment would be worth almost $1.6 million, even though you contributed only $120,000 over the period. This is an oversimplified example, but you can see the possibly life changing effects of money making money for yourself using this tool created by the Australian Government, especially when given time to work. You can see this for yourself by reducing the “Number of years” in the tool to 45, while keeping the initial and regular deposit at 200, along with the interest at 8%, equivalent to starting to invest just 5 years later.

This is why, one of the biggest and most common regrets of investors is not starting earlier, due to the compounding effect. An awesome video explaining these fundamental concepts with more examples!

Retiring Early?

With the increasing awareness of this wonder, has come the rise of the Financial Independence Retire Early (FIRE🔥) movement. Being able to gain “financial independence” by saving more than the average person, can allow you to build a “nest egg” of investments when you’re young, especially due to compounding. This can then give you the opportunity for you to spend more time working on things that give you more fulfillment, whilst still earning a passive income.⁶

Compounding Knowledge

Like money, knowledge also compounds. If you spend just 10 minutes every day or so to read a blog like this or listen to a podcast about personal finance, this can pay off dividends in the long run. And once you become more confident in your knowledge, you might be able to help others around you improve their financial situation — like I’m trying to do now!

Supporting your Values

If the idea of compounding didn’t float your boat, then maybe upholding your moral code will. Over the past few years, there has been the rise of Environment, Social and Governance (ESG) investing, which focuses on assets that aim to have a more positive impact on the planet and people, through the better management of stakeholders such as the board of directors and employees. Through ESG investing, you can support companies that you truly believe are creating a better world for yourself and for humanity (consider Microsoft, which aims to be carbon negative by 2030). Not to get too technical in how this process works, but as more people want to own shares of an ESG company, this can allow them to raise more money, allowing them to have a greater impact.

Some things to keep in mind before you invest

I am not a financial advisor by any means, please keep in mind these are just general guidelines. This list is not exhaustive and I encourage you to do your own research to make sure investing is right for you at this point in time.

- Pay off your ‘bad debts’ first — These are usually high interest loans such as overdue (interest yielding) credit card and BNPL debt, as well as loans on depreciating assets (things that generally decrease in value when bought), such as a new car. If you were to not pay off these debts which often have over 10% interest, you would be eroding the gains from your investments which are often less than that.

- Have an emergency fund — This is money in a savings account that you can easily access in case of an emergency (e.g. you lose your job unexpectedly, you need to do essential repairs on your car). This is important as if you had almost all your money invested and needed to cash it out urgently, this usually comes with having to pay more capital gains tax (when you make a profit) and the money taking at least a couple of days to transfer. The general guideline is to have at least 3 months of living expenses in the emergency fund. For young people still living at home, this is not as essential but it’s generally good to have at least some cash available.

- Investing does not generally do well in the short term — In the investing approach I will describe in Parts 2 and 3, the consensus of professional investors is that you need to be able to keep this money invested in the long term (i.e. 10+ years) in order to receive benefits such as compounding and overcoming short term volatility. So if you’re saving up for something like a deposit for a house in the next few years, investing that money through this approach is generally not advised, as there is a chance that there might be short term losses, but this shouldn’t be a concern if you’re investing for the long term.

What are the next steps?

This post is the first in a series that will build upon the financial concepts covered here, with more practical examples and actionables.

Keep an eye out for Part 2 of this series, which will go into the framework for investing that I think is best for most people, called ‘passive’ or ‘long-term’ investing.

Part 3 will cover the asset which I think is best for people to follow this investing approach, namely Exchange Traded Funds (ETFs), including how to buy them and a shortlist of some ETFs to consider purchasing.

¹ A good podcast series deep-dive if you want to learn more about the types of assets here

² It was surprisingly hard to find a resource which goes into more detail about this fundamental concept. The best I could find is the“ “How investments can earn you money” of this article.

³ A more detailed explanation on this distinction in this video (also many other good introductory and topical videos here).

⁴ This article is not up to date with the current situation, but is still relevant, going into a bit more detail into inflation.

⁵ More on how you can buy an asset that tracks the price of the stock market in part 3, but keep in mind this rate is by no means guaranteed, especially in the short term.

⁶ A video explaining more about the FIRE movement.

I really appreciate you getting all the way to the end! If you have any questions, suggestions, corrections or any sort of feedback on my first article, I’d be more than happy to hear it! Best way to get in touch if you haven’t already, is to connect with me on LinkedIn linkedin.com/in/ethan — wong or email me at ethanwong12@protonmail.com.

Disclaimer

All content provided in this post is for general information purposes only, and should not be constituted as professional advice. Ethan Wong is not a financial adviser, and you should consider seeking professional advice to understand how this content relates to your individual circumstances. Ethan Wong is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by use of this content.